Financial Market Breakdown –

Week of August 8, 2022

Share

Quick Highlights

Futures are slightly higher thanks to solid Chinese economic data and following a mostly quiet weekend.

Chinese exports rose more than expected (18% vs. (E) 14.1%), helping to slightly improve global economic sentiment.

Politically, Senate Democrats passed the Inflation Reduction Act over the weekend as expected, and it should become law this week. But, markets don’t expect any meaningful impact on corporate earnings in the near term.

What’s Happening in the Financial Market?

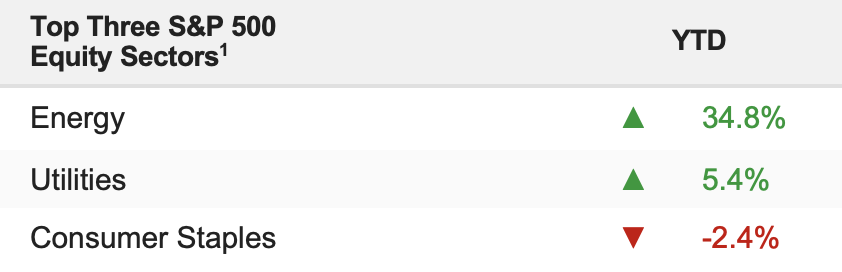

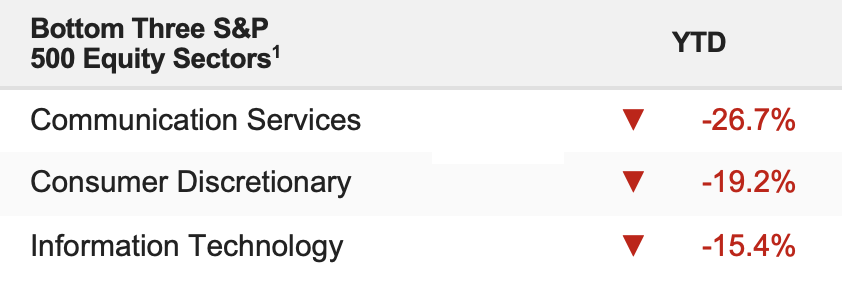

Stocks were resilient last week, holding midweek gains driven by easing geopolitical fears and Goldilocks economic data through Friday’s very hot July jobs report. The S&P 500 gained 0.36% on the week and is down 13.03% year to date.

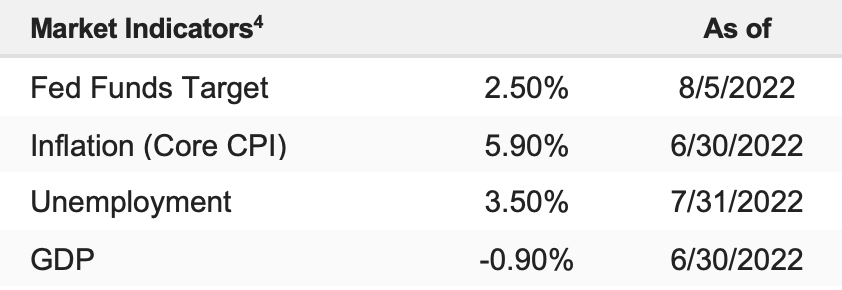

Friday’s jobs report came in much hotter than expected, and the net impact of that report is to make this Wednesday’s CPI report even more important. If that report does not signal a peak in inflation, then this market will very likely suffer at least a moderate pullback.

Notably, stocks on Friday were resilient in the face of the much-better-than-expected jobs report as markets didn’t decline materially despite the bond market now pricing in a 75-bps rate hike in September (vs. 50 bps previously). The reason for that resilience, as we and others suggested, was the looming CPI report. That’s because if CPI does signal a peak and decline in inflation, the bulls will have a quasi-compelling story.

Consider that last week’s data (PMIs, jobs report) shows the U.S. economy is resilient and not materially losing momentum, and that’s good for corporate earnings. Q2 earnings season has come in better than feared, and 2023 expected S&P 500 EPS are between $230-$240, much higher than feared. So, if inflation is really peaking and if we get to peak Fed hawkishness by the September meeting, then we can honestly say the chances of a “soft” economic landing will increase, and the recent gains in stocks could be justified on a fundamental basis.

But there’s a problem. The bond market is screaming we are headed for an economic contraction that hasn’t even started yet. The economy hasn’t even begun to feel the impacts of rate hikes and full Quantitative Tightening. By September, the FOMC will have hiked 300 basis points in six months. Rate hikes take time to filter through the economy. Normally, it takes years for 300 bps of tightening. Now it’s occurred in six months. There’s a delay on when that tightening actually:

Reduces consumer spending

Reduces corporate profits

Causes layoffs (which impacts spending and profits)

Bottom Line

Yes, if CPI peaks and the Fed signals peak hawkishness in September, those are positive events. But the economy still has to digest all this tightening, which will materially slow things. That hasn’t even started to occur yet, so celebrating the resilience of earnings and economic data when we’re still in an expanding economy (regardless of the GDP prints) seems to be the equivalent of a coach declaring victory because the game plan should work. Game plans are great, but things change once the game starts, and the “game” of the slowing U.S. economy (which is needed to slow inflation) hasn’t even started yet—we’re still in warmups.

Near-Term General U.S. Stock Market Outlook

Near-Term (1 month) Stock Market Outlook: Neutral

Stocks were little changed last week as markets digested solid economic data (ISM PMIs and Jobs Report) combined with more signs of a peak in inflation as investors look ahead to this week’s CPI report.