Financial Market Breakdown –

Week of August 23, 2022

Share

Quick Highlights

Stock futures are steady this morning as this week’s rise in both the dollar and bond yields has paused while European economic data was better than feared.

Economically, the Eurozone Manufacturing PMI was 49.7 vs. (E) 49.0, and the Services PMI came in at 50.2 vs. (E) 49.0, which is helping ease some stagflation concerns.

Econ Today: PMI Composite Flash (E: 49.2), New Home Sales (E: 575K).

What’s Happening in the Financial Market?

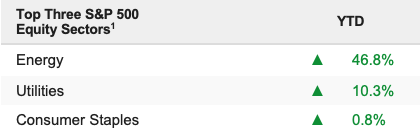

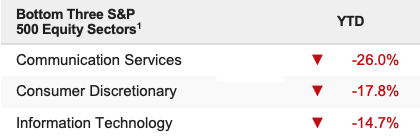

Equity markets wavered between gains and losses before ending the week with a loss as investors continued to assess the future path of Fed policy amid mixed economic data. At the same time, a sizeable options expiration weighed on stocks into the weekend. The S&P 500 fell 1.21% on the week and is down 11.28% YTD.

Stocks dropped last week, and the reason for the decline reflects the current setup in this market, as nothing really “bad” happened last week, but it didn’t have to as the S&P 500 has priced in a lot of future positives occurring—and that’s not a guaranteed outcome. Put differently, the issue with this market isn’t so much the fundamentals as it is the assumptions and valuations.

Fundamentals have improved since July, earnings were more resilient than feared, and inflation has peaked and will likely decelerate in the coming months. The Fed will likely begin to ease off rate hikes between now and year-end. All of those things are positives compared to where the market was in early July.

The problem, however, comes from valuations and assumptions. At 4,228 (Friday’s close), the S&P 500 is trading at a 17.6X multiple on $240 2023 S&P 500 earnings. For the market to have more upside risk than downside risk from here, that means we must assume:

Earnings don’t decline from the $240 expectation. That means there will be essentially no macroeconomic slowing.

No recession or material growth slowdown. A 17X- 18X multiple is only appropriate in an environment of solid economic growth. Typical recession contraction forward multiples are 15X or lower!

The Fed really does turn dovish in 2023. Again, a 17X -18X multiple assumes that the Fed will not only stop hiking but begin easing policy next year.

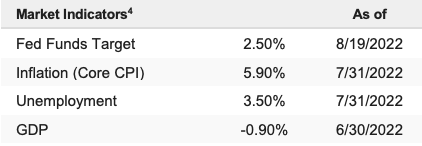

Inflation does quickly recede. It’s great that inflation has likely peaked, but it’s still at 8% YoY. It’s supposed to be 2%. If it doesn’t move quickly towards that target, then the Fed will have no choice but to keep raising rates above the current 3.5% terminal rate expectation.

Now, could all these things happen? Absolutely—and in this scenario, the Fed would perfectly “stick” an economic soft landing, and we can all look forward to new highs in the S&P 500 sooner than later.

Bottom Line

While past history is not indicative of future results, we want to continue bringing up one main point: The economy is not slowing yet. There is virtually no economic pain due to rate hikes or QT. Job openings are still 10MM vs. typical 7MM. Unemployment is sub 4%, and no economic indicators are flashing warning signs yet.

But if the economy does slow in the next several months, then assumptions 1 and 2 will be proven false. In that instance, we should easily expect a 5%-10% pullback as markets reprice a less perfect future macro outcome.

For these reasons, we continue to advocate holding longs (the good outcome is possible) but overweighting low-beta and defensive sectors to insulate against the possibility that the Fed does not pull this off.

Near-Term General U.S. Stock Market Outlook

Near-Term (1 month) Stock Market Outlook: Neutral

Stocks dropped modestly last week despite solid economic data, as markets digested the recent rally and considered the expectation that the Fed really will get materially less hawkish in the coming months.