Financial Market Breakdown – Week of July 25, 2022

Share

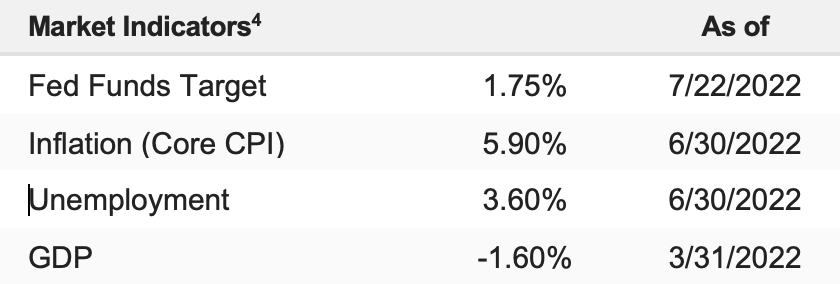

Quick Highlights

Futures are modestly higher as markets bounce from Friday’s declines, following a quiet weekend and as investors look forward to numerous important catalysts this week.

Chinese authorities are considering some restrictions on movement in Shanghai as COVID cases rise but are still resisting broad lockdowns (for now).

Economically, German Ifo Business Expectations declined further (80.3 vs. (E) 83.3).

Econ Today: Chicago Fed National Activity Index (E: 0.05).

Last week’s price action accurately reflects the near-term dynamic in this market:

Rising anecdotal evidence of a peak in inflation (Empire prices indices, UM Inflation Expectations, Philly Price Indices) combined with extremely pessimistic sentiment pushed stocks to six-week highs. But the market fell on Friday as it was forced to confront the negative impacts of slower growth via a series of bad earnings reports (SNAP, STX, VZ) and slowing economic momentum (the flash PMIs). Going forward, it’s going to be the push/pull of peaking inflation vs. slowing growth/declining earnings that will determine if the rally continues or rolls over.

More specifically, if we assume that peak inflation is here (and frankly, that’s an aggressive assumption given we only have anecdotal evidence of peaking inflation), then two key questions will determine whether the S&P 500 can rally towards (and maybe through) 4,100, or roll back over and drop into the mid-to-high 3,000s:

How quickly does inflation subside?

How much does growth slow?

The first question matters because, as we and others have said, inflation not only has to peak but also rapidly decline if the Fed is going to stop hiking rates. Practically, CPI can peak in August, but if it’s November and year-over-year CPI is still above 7%, the Fed can’t announce a “pause” in rate hikes (CPI would still be more than double the upper limit of 3%).

The second question matters because inflation can drop. Still, if the economy hits a hard stall and we’re in a material contraction in the third or fourth quarter, then earnings will drop further, and markets will be searching for Fed rate cuts (something not likely for at least a year).

Bottom Line

The idea of peak inflation has (mostly) underwritten this recent rally in the S&P 500. However, even if it’s true that inflation has peaked (we won’t know till the August 10 CPI report, and if it doesn’t show a peak, then stocks should drop, possibly hard), that isn’t a silver bullet to end the volatility.

For this market to move substantially higher and have those gains underwritten by improving fundamentals, we need to see:

Peak inflation

A rapid decline in inflation

A mild moderation of growth

Markets rallied on the first possibly coming true, but the second and third will be tricky and, at a minimum will keep volatility elevated.

Near-Term General U.S. Stock Market Outlook

Near-Term (1 month) Stock Market Outlook: Neutral

Stocks rallied hard last week as more evidence appeared that inflation has potentially peaked. However, disappointing economic growth data on Friday saw some mild giveback of the early week gains.