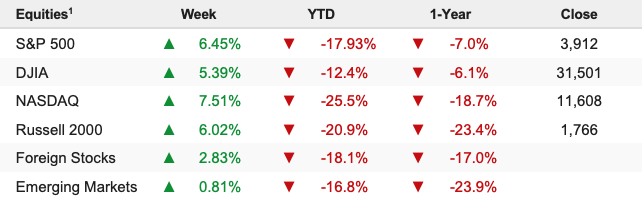

Stocks rallied, and bond yields pulled back from recent highs last week as economic data suggested the Fed’s tightening actions have already impacted growth which ultimately brought forward expectations for “peak hawkishness.” The S&P 500 surged 6.45% on the week and is now down 17.93% YTD.

Stocks rallied solidly last week and bounced back from the post CPI collapse, thanks primarily to the notion that we may be getting closer to peak inflation and peak hawkishness from the Fed than was previously expected.

The reasons for that optimism were a sharp decline in numerous commodities (including copper, wheat, oil, and natural gas), underwhelming flash PMIs, growing anecdotal evidence to imply the U.S. economy is losing momentum, and revised University of Michigan Inflation Expectations that saw five-year inflation estimates drop to 3.3% to 3.1%.

Positively, a continued decline in commodities prices and further moderation in economic activity has the potential to push inflation lower in the coming months. If that happens, then we’re closer to “peak hawkishness” from the Fed than was assumed following the much-hotter-than-expected CPI from two weeks ago.

While we certainly enjoyed last week’s rally in stocks, it’s important to realize that, at this point, investors are mostly “grasping at straws” on-peak inflation and peak hawkishness. Yes, commodities are declining, and the economy is moderating. Still, it’s unclear how quickly that will translate to materially lower CPI, which is what the Fed needs to be able to back off its increasing hawkishness.

Last week’s rally was solid and the S&P 500 is acting better on a technical level (we closed above 3,800). Over the coming several weeks, there is a chance to see a real moderation in inflation pressures (which would come via a continued decline in commodity prices and moderation in economic activity). If that happens, stocks can continue to rally as it gets us closer to fulfilling one of our “Three Keys to A Bottom.”

However, we do need to point out that so far this year, every time markets have priced in a “peak” in inflation, it’s not worked out and just set up for more disappointment— so while we certainly hope this time the peak is “real” we want to point out there’s not much evidence of it yet. So, until there’s more concrete evidence of a peak in inflation and peak in Fed hawkishness, we view this as merely another bounce and not a market bottom (for that to occur, we still need: 1) Peak inflation/peak hawkishness, 2) Full China reopening and 3) Relative geopolitical calm. None of them are in place right now).