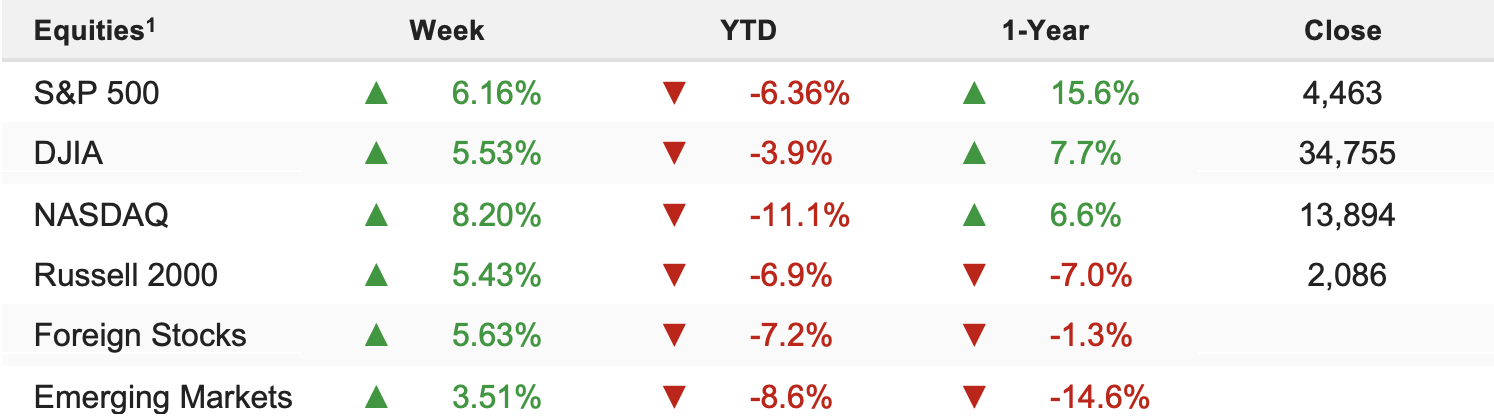

Stocks rallied the most since the 2020 election last week as traders digested the first Fed rate hike in more than three years, mixed economic data, and ongoing hopes for a ceasefire in Ukraine. The S&P 500 surged by 6.16% on the week and is now down just 6.36% YTD.

The impact of geopolitical tensions in Eastern Europe is beginning to fade as the market still expects a ceasefire at some point while the conflict has yet to spill outside of Ukraine. That is not to say that the invasion of Ukraine has not been a terrible human tragedy with an unneeded loss of life, which we fully acknowledge. However, markets are no longer pricing in the prospects of the conflict spreading to neighboring nations or escalating to the point where nuclear weapons might become a real threat, which was the initial source of fear surrounding the conflict.

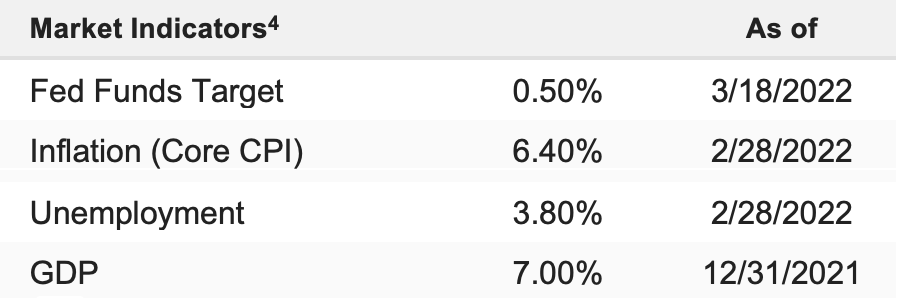

As such, investors refocused on economic data and central bank policy expectations last week and while the Fed was hawkish in releasing its dot plot, which is forecasting seven rate hikes this year, the market didn’t “buy it”—especially considering the lower revisions to economic growth expectations and higher revisions to inflation forecasts. That was evident in the fixed-income markets, which dialed back rate hike expectations for 2022 and began pricing in rate cuts in 2023 as odds of a policy mistake were seen as rising sharply.

That was also an appropriate response from the market as it’s hard to present an argument for hiking rates when you believe growth is slowing significantly. As such, there are three things we need to monitor in the near term to have a well-founded outlook for equities in the months and quarters ahead: market-based rate hike expectations, economic data, and the 10s–2s yield spread.

While we’re cautiously optimistic that stocks are in the process of putting in a near-term bottom and stabilizing in the fundamental trading range of 4,300 to 4,600 in the S&P 500, that thesis would be broken by:

A significant hawkish shift in rate hike expectations, which would indicate a likely policy mistake in the months ahead.

An acceleration in economic growth data that could lead the Fed to hike more aggressively (potentially with 50-bps hikes at coming meetings), which also would raise the odds of a policy mistake.

An inversion in the yield curve that would suggest the Fed has already made a policy mistake. If any of these developments occur near term, we will need to begin planning for more defensive positioning given the rising odds of a looming recession.

Bottom Line

For now, we continue to favor value exposure over growth and higher inflation/rate sectors including commodities (XLE) oil. That positioning stance will likely continue until we see one of the three factors listed above shift and signal a change in the outlook for economic growth and subsequent Fed policy decisions.

Near-Term General U.S. Stock Market Outlook

Near-Term (1 month) Stock Market Outlook: Neutral

Stocks stabilized last week amid perceived progress in the Russia–Ukraine ceasefire talks and a strong push into risk assets following the Fed meeting, as traders doubted the FOMC’s plans to raise rates so aggressively this year. The S&P 500 had its best week since the 2020 election, which was at least partially amplified by quadruple witching options expiration on Friday.