Financial Market Breakdown – Week of March 14, 2022

Share

Quick Highlights

U.S. stock futures are trading higher with European shares amid renewed hopes of a ceasefire in Ukraine while Asian markets declined overnight on new Covid-19 lockdowns.

Geopolitically, Russia continued with aggressive military attacks against Ukraine over the weekend but diplomatic negotiators noted solid progress in ceasefire discussions which is helping risk assets bounce this morning.

What’s Happening in the Financial Market?

Stocks remained volatile last week as investors continued to monitor the status of the Russian invasion of Ukraine and a few key economic reports. The S&P 500 dropped 2.88% on the week and is down 11.79% YTD.

Stocks dropped again last week, but despite the decline it’s fair to say that it could have been worse. The negative headlines last week were incredibly consistent: Continued escalation in the Russia/Ukraine war, hawkish surprise by the ECB ending QE in Q3 (sooner than expected), inflation hitting

yet-another 40-year high and commodity prices exploding higher. And those were just the majorly

negative headlines (we’re not including negative commentary from companies such as Booking.com, the renewed implosion of Chinese shares on delisting fears, higher yields despite growth headwinds).

Yet despite all that, the S&P 500 didn’t fall to fresh lows, and we think that’s notable. More specifically, this market could be setting up for a near-term rally if we get any good news, e.g. a lasting ceasefire in Ukraine, the Fed not being as hawkish as feared, positive supply news on oil, etc. And that rally could easily send stocks back to the 4,500-4,600 range in part because sentiment has become so palpably negative.

But while we’d certainly welcome that rally, it wouldn’t change the fact that the outlook for stocks remains challenged over the coming month, and that was the case before the Russia/Ukraine situation. Point being, if we get some resolution there, it’s not a material bullish catalyst. For a rally to be sustainable towards the new highs we need to see 1) The Fed be very gradual in rate hikes and, more importantly, Quantitative Tightening, 2) Inflation peak and recede, 3) Corporate earnings hold steady and 4) Geopolitical calm. At this point, none of those things are more likely than not!

Bottom Line

The market is resilient, and we think that’s important, and we could see a solid rally if we can just get some good news. But there remain numerous head- winds on the markets and as a result we continue to view the S&P 500 is a 4,600-4,300ish band as long as the Fed isn’t too hawkish, the Russia/Ukraine conflict doesn’t expand to NATO, and there are no other material negative surprises.

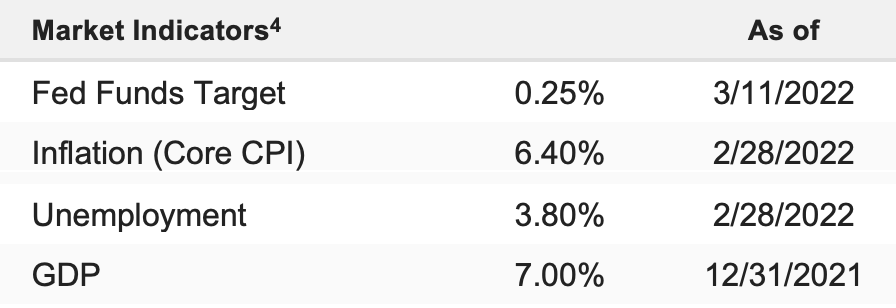

From a Fed standpoint, last week’s CPI and the previous week’s jobs report likely ensure we get a 25-bps hike on Wednesday, but it will not diminish the Fed’s hawkishness, and as a result it remains unknown how many rate hikes the “dots” will show in 2022 (CPI and the jobs report likely didn’t lower that number).

Looking forward, markets will continue to wait for a peak in inflation, because only after that peak can we expect the Fed to start to get less hawkish, and especially given commodity prices, that likely isn’t happening anytime soon, even if we see a slowing in growth (which we likely will in the coming months).

Bottom line, the takeaways from last week were clear: Inflation remains very, very high and we have not yet seen a peak in inflation pressures, and global central banks remain committed to tightening policy even given risks to growth, further reinforcing that rates are going higher and central banks are not the same as they have been for the last 10 years (where rates were cut at the hint of slowing growth) and that will keep market volatility high, and be a headwind on stocks returns.

Near-Term General U.S. Stock Market Outlook

Near-Term (1 month) Stock Market Outlook: Neutral

Stocks dropped again last week as the Russia/Ukraine war further intensified, sending commodity prices soaring and increasing the chances of a future slow- down in economic growth. The longer the conflict goes on, the greater the head- wind it will become on stocks.